Answer:

owkaowowooaoaoaoaooaoaoaooaoaooaoaoaooa

Explanation:

aooaoaoaoaooaoaoaoaooaoaoao

Answer:

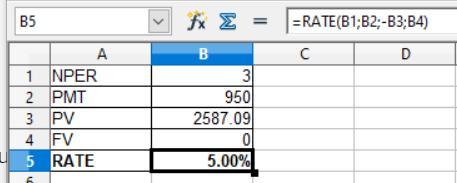

1. 5.00%

2. 15.70 year

Explanation:

As per the data given in the question,

1) For computing the interest rate we need to applied the RATE formula which is shown in the attached spreadsheet

Given that

Future value = 0

Present value = -$2587.09

PMT = $950

NPER = 3 years

The formula is shown below:

= RATE(NPER;PMT;-PV;FV)

The present value comes in negative

After applying the above formula, the interest rate is 5%

2) For computing the number of years we need to use NPER i.e to be shown in the attachment below

Given that

Future Value = $920,925

Present Value = 0

PMT = -$40,000

Interest rate = 5%

The formula is shown below

= NPER(RATE;-PMT;PV;FV)

The PMT comes in negative

After applying the above formula, the nper is 15.70 years

Answer:

8.13%

Explanation:

Annual return = [ (Total FV/Initial investment)^(1/n) ] -1

n = useful life of the project

Total Future Value = (22650*5) +5000

Total FV = $118,250

Initial investment = $80,000

Annual return = [ (118,250/80,000)^(1/5) ] -1

r = [ (1.478125^(1/5)] -1

r = 1.0813 - 1

r = 0.0813 or 8.13%

<span> Manufacturing overhead describes the difference between manufacturing overhead cost applied to work in process and manufacturing overhead cost actually incurred during a period.</span>

Over-applied manufacturing overhead would result if the manufacturing overhead cost applied to work in process is more than the manufacturing overhead cost actually incurred during a period. So, in over-applied overhead the applied overhead is bigger than the actual overhead.