Answer:

E. Debit Retained Earnings $7,400; credit Common Dividends Payable $7,400.

Explanation:

The Journal entry is shown below:-

Retained earnings Dr, $7,400 (14,800 × $0.50)

To Common dividend Payable $7,400

(Being dividend declaration is recorded)

Here to record the dividend declaration we simply debited the retained earnings as it decreased the stockholder equity and credited the common dividends payable as it increased the liability

So the correct option is D.

Answer:

$8,000

Explanation:

Income distribution deductions apply only to an estate or trust's distributable net income (DNI). In this context, the beneficiaries of an estate or a trust are taxed directly based on the money distributed to them. That means that the estate or trust can deduct distributions when calculating taxes. This is done to avoid double taxation, since the beneficiaries are taxed, then the estate or trust is not.

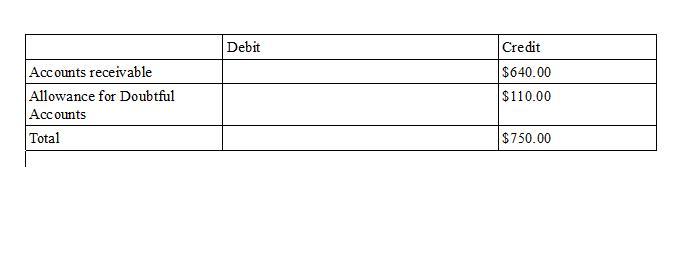

Answer: <u><em>The adjusting entry at the end of the year will include a credit to Allowance for Doubtful Accounts in the amount of: $750</em></u>

Given:

Accounts receivable = $640

Allowance for Doubtful Accounts = $110

<em><u></u></em>

<em><u>Therefore, the correct option is (c).</u></em>

The yield of maturity for this bond is "8.4 percent".

We can calculate this in the following way;

<span>Yield to maturity = YTM = {($1,000 x .06) + [($1,000 - 900)/5]}/[($900 + $1,000)/2]

=(60 + 20) / (950)

=80/950

=0.084

=0.084 x 100

= 8.4 percent</span>