A: raises

B: lowers

c: does not change

I would put B as the answer because the government helps control the price so everyone can rent an apartment.

Answer:

to keep track of all business transactions in case of an audit

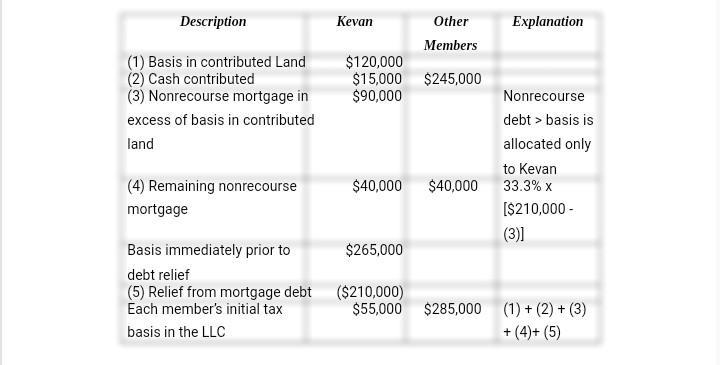

Answer: A: $0.None of the members recognize gain because their debt relief was not in excess of their bases in their LLC interest prior to any debt relief.

B: $55,000

C: $285,000

D: $625,000 Albee, LLC takes a $135,000 carryover basis in the assets Kevan contributes and a $490,000 basis in the total cash the other two members contributed.

Explanation: check attached file

First three together in the first I think

Answer:

Please check the answer below

Explanation:

a. One issue is the "locking-in" of assets. If I hold shares of Corporation X, then I can delay paying taxes as long as I don't sell. Effectively, I get to keep all of the interest/dividend payments on my tax liability. However, if I discover that X is really a poor investment and Corporation Y is better, then selling X and buying Y means that I have to pay taxes. This might discourage me from making a switch to a more profitable/efficient investment decision. This is the "locking-in" effect.

b. A short-run cut might cause many people to sell stocks that they had felt "locked-in" with. The penalty for switching is smaller, so more people will do it -- resulting in a great deal of cap gains tax revenue collected.

c. Taxing realized gains, even when the stock is not sold, rather than just accrued gains would eliminate this locking-in effect. Investors would not be penalized for switching to a better investment, and long-term capital gains revenue (as well as efficiency) would rise.