rating expense item. Hossa's income tax rate was 22% in 20X1 and 24% in 20X2

2011 2012

($ in millions) ($ in millions) of sales % ($ in millions) of sales % Sales

Cost of sales $5,500.0 $6,500.0

Other operating expenses (2,475.0) 45% (3,055.0) 47%

Operating income (825.0) 15% (1,040.0) 16%

Provision for income taxes 2,200.0 2,405,0

Net income 484.0 (577.2)

Income tax rate $1,716.0 $2,827.8

22% 24%

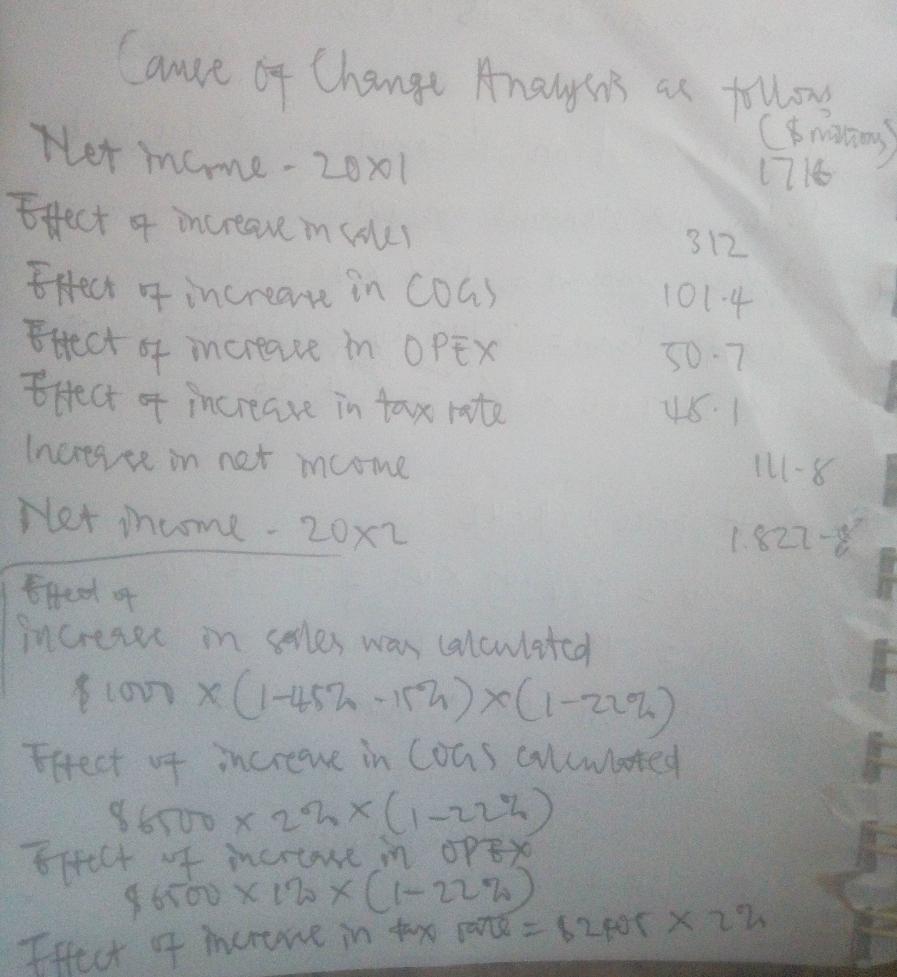

Hossa’s management was pleased that 20X2 net income was up 6.5% from the prior year. Although you are also happy with the increase in net income, you are not so sure the news is all positive. You have modeled Hossa’s income as follows:

NET INCOME = SALES × (1 − COGS% − OPEX%) × (1 − TAX RATE)

Using this model, net income in 20X1 is computed as $5,500 × (1 − 45% − 15%) × (1 − 22%) = $1,716.0. Net income in 20X2 is computed as $6,500 × (1 − 47% − 16%) × (1 − 24%) = $1,827.8.

Required:

Prepare a cause-of-change analysis to show the extent to which each of the following items contributed to the $111.8 million increase in Hossa’s net income from 20X1 to 20X2: (Do not round intermediate calculations.

Increase in sales (SALES)

Increase in cost of sales as a percent of sales (COGS%)

Increase in other operating expenses as a percent of sales (OPEX%)

Increase in income tax rate (TAX RATE)